Broadcom Drops 14%: Is the AI Market Rotation Real?

By SCAD3D Insights

- Broadcom

- AVGO

- AI Market Rotation

- AI Stocks

- Nvidia

- AMD

- AI Chip Selloff

- Priced for Perfection

- Sector Rotation

- Stock Market 2026

- AI Bubble

- IPO Supply

Broadcom dropped 14% on 4 June after beating earnings. Nvidia is up 19% YTD while AMD is up 143%. Is this the start of AI market rotation, or just a buy-the-dip moment?

Broadcom beat earnings on 4 June and still fell 14%. Nvidia is up around 19% year-to-date. AMD is up roughly 143%. Intel is up 192% from a low base. The S&P 500 has managed about 10%.

That is not a dying AI trade. It is a rotating one. And the rotation is happening inside the AI complex itself, not from AI into safety.

Applying the 3D Framework

-

Direction: The AI story is still alive. Compute demand, data-centre buildout, electrification and enterprise adoption are all expanding. What is changing is that the AI king is no longer the only winner. In 2026 Nvidia has actually been the laggard among major chip names.

-

Depth: Money is moving inside the trade. AMD, Intel, Lumentum, Applied Materials and Micron-type suppliers are getting the next premium. Anyone who owned the broad AI label did well in 2024 and 2025. Anyone who only owned the single most crowded name is being punished now.

-

Downside: The bigger risk is supply, not sentiment. OpenAI is reportedly targeting a $1 trillion valuation on around $25 billion in revenue while losing roughly $14 billion this year. Other large private AI names are also nearing the public market. That new supply has to be funded by trimming something. Usually the most crowded mega-cap positions.

What Broadcom Told Us

Broadcom did not miss. It beat. The stock still dropped 14% because the guidance was steady rather than spectacular, and the P/E was already above 90.

That is the new mood. Beating estimates is no longer enough. The bar is the guide, the margin path and the capex story. Companies that grow into rich valuations get rewarded. Companies that merely meet a high bar get sold.

A year ago that would have been a buying opportunity. Now it is a warning.

Where The Money Is Going

The first phase of the AI trade rewarded belief. Anyone who bought AI broadly did well.

The current phase rewards specificity. AMD is gaining on data-centre EPYC and Instinct demand. Lumentum sells optical and photonic components into AI infrastructure. Applied Materials sells the capital equipment that builds the chips. Intel is running off a depressed base but is still part of the same picks-and-shovels logic.

None of these were the consensus crowd trade twelve months ago. That is the point. Investors who already own Nvidia at full valuations are looking around the supply chain for places where expectations are lower.

The Bear Case Against Rotation

A serious post should test its own thesis.

Nvidia's last quarter was strong. The Computex announcements reframed it as a consumer-AI story as well as a data-centre one. Intel's YTD performance is partly a low-base effect, not durable earnings power. A clean Oracle Q4 on 16 June, a dovish first Fed meeting under Chair Warsh on 17 June and a confident Nvidia AGM on 24 June could easily put the original leadership back in front.

A single bad day for Broadcom is not a regime change. It is one data point.

Takeaway

The AI trade is not over. It is becoming more selective.

The structural case is intact because compute, power and enterprise adoption are all still expanding. What has changed is that the easiest phase, when the label alone was enough, is behind us.

The better question is not whether AI is finished. It is whether the AI exposure in your portfolio is still being paid for the right reasons. Owning the king at any price worked from 2023 to 2025. It is not obviously the strategy that works from here.

Rotation rarely kills bull markets. But it does punish concentration.

Risk Notes

Market rotation is difficult to time. AI leadership can reassert itself quickly, and short-term performance data can mislead about long-term value.

Nothing here is financial advice or a recommendation to buy, sell or trade any security. The tickers mentioned are research starting points, not recommendations. Do your own due diligence and speak with a licensed advisor before making investment decisions.

Found this useful?

Source note: Based on public market data from 4 June 2026, Broadcom earnings reaction, semiconductor sector performance, IPO pipeline coverage and SCAD3D 3D Framework analysis.

Disclosure: SCAD3D Insights holds no position in the mentioned assets at the time of publication.

More Insights

NVIDIA vs Dell: The AI Infrastructure Trade Explained

NVIDIA captures the highest-margin layer of the AI boom. Dell shows how much of that demand is becoming real servers, racks and data-center infrastructure.

- NVIDIA

- NVDA

- Dell

- DELL

- AI Infrastructure

- AI Servers

- Data Centers

- Semiconductors

- AI Chips

- AI Compute

Copper Market 2026: Supply Squeeze, EV Demand and How to Invest

Copper prices are rising because the world needs more electricity, EVs, grid upgrades and data centres, while supply remains tight. Here is the copper thesis in plain English.

- Copper

- Copper Price

- Copper Investing

- Copper ETF

- Copper Miners ETF

- CPER

- COPX

- Boliden

- Aurubis

- EV Demand

- Energy Transition

- China Copper Demand

- Copper Physical Premiums

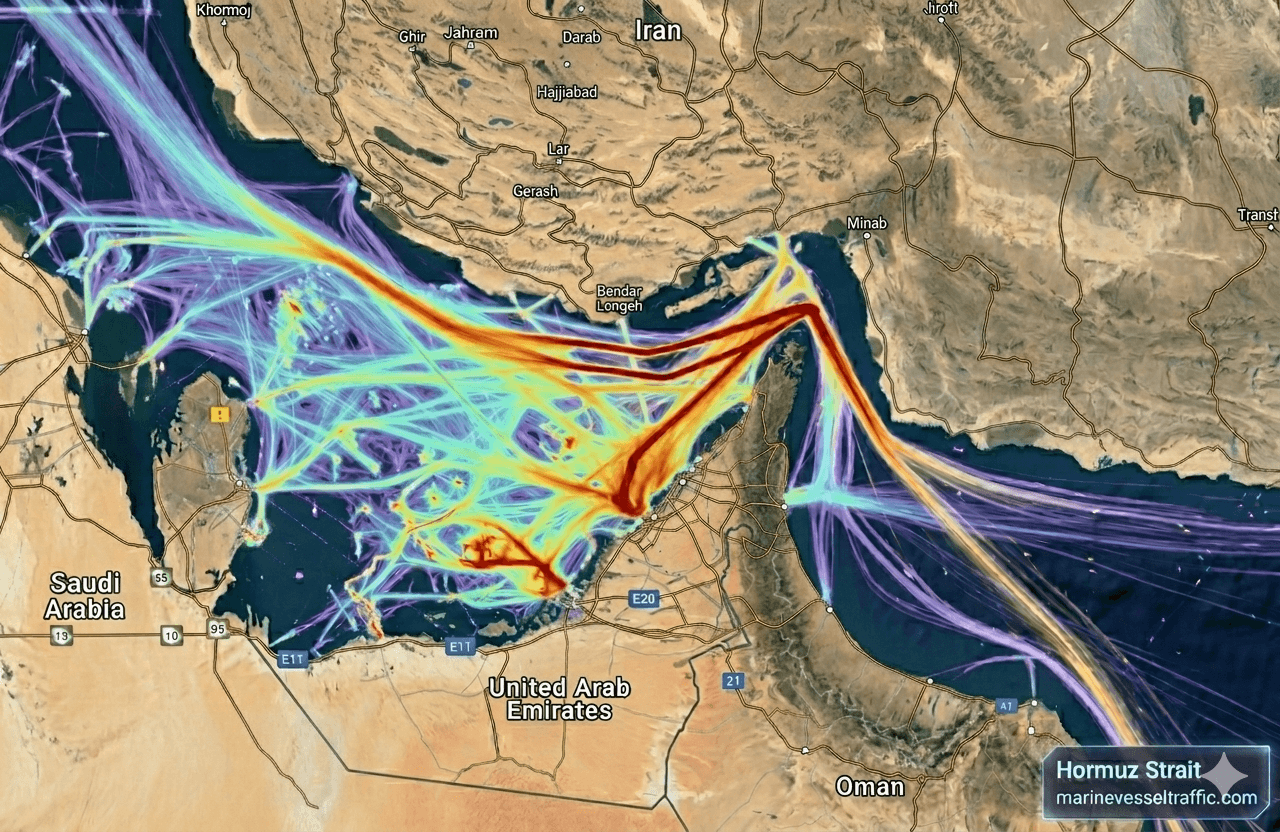

Strait of Hormuz Crisis 2026: Oil, LNG and Cost Shock

The Strait of Hormuz crisis is not just an oil story. It is an illegal war, a fight for control, and a global cost shock hitting fuel prices, LNG prices, shipping, inflation and markets.

- Strait of Hormuz

- Hormuz crisis 2026

- Hormuz closure

- US Iran war

- oil prices

- Brent crude

- LNG prices

- tanker stocks

- war risk insurance

- energy inflation

- global supply chain