Strait of Hormuz Crisis 2026: Oil, LNG and Cost Shock

By SCAD3D Insights

- Strait of Hormuz

- Hormuz crisis 2026

- Hormuz closure

- US Iran war

- oil prices

- Brent crude

- LNG prices

- tanker stocks

- war risk insurance

- energy inflation

- global supply chain

The Strait of Hormuz crisis is not just an oil story. It is an illegal war, a fight for control, and a global cost shock hitting fuel prices, LNG prices, shipping, inflation and markets.

The Strait of Hormuz crisis 2026 is not just an oil story.

It is not just about Brent crude, LNG prices, tanker stocks or war risk insurance.

It is about an illegal war turning into a global cost shock.

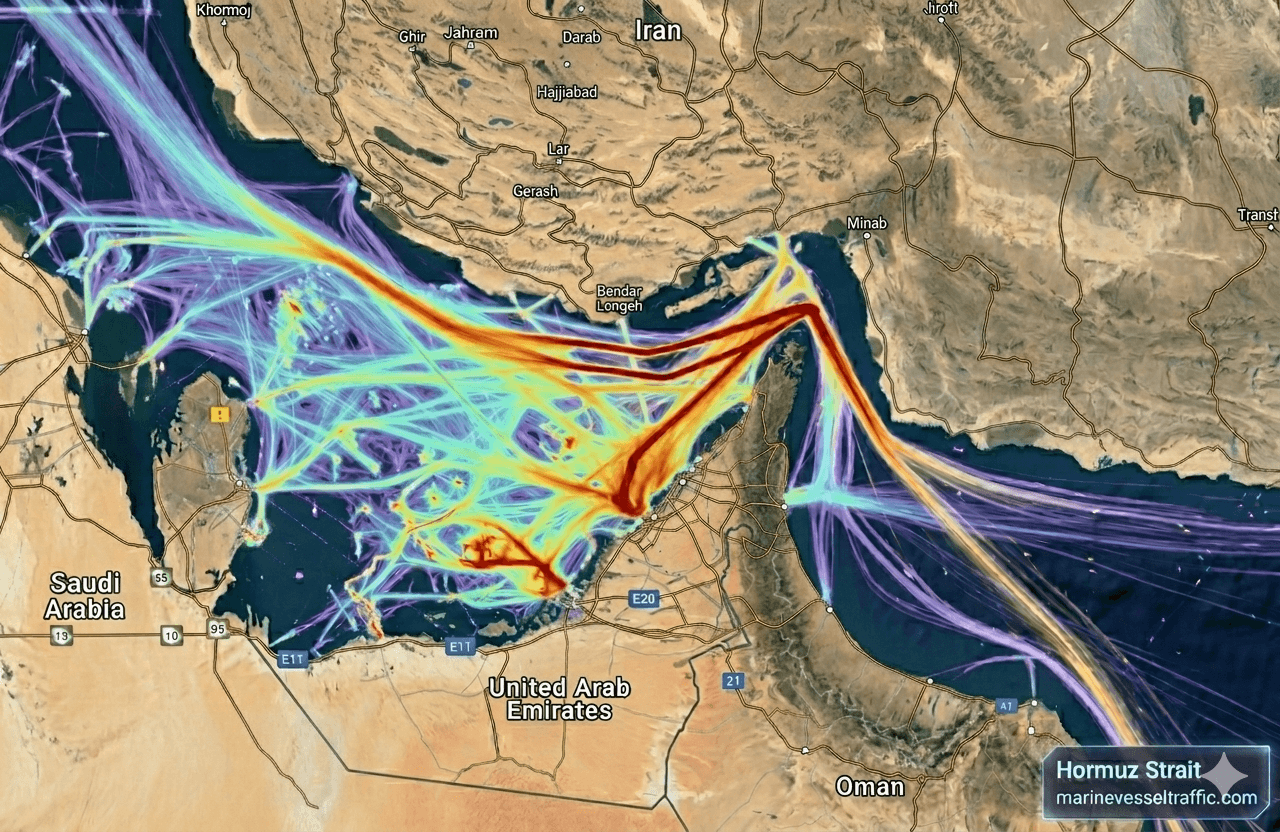

The Strait of Hormuz is only about 21 miles wide at its narrowest point. Yet it carries around 20 million barrels of oil and petroleum products per day. It also carries about one fifth of global LNG trade.

Most people never think about it.

Now they are paying for it.

Fuel prices. Airline tickets. Food transport. Factory costs. Fertiliser. Plastics. Household energy bills. Currency pressure. Central bank decisions.

This is how war travels.

Not only through missiles.

Through invoices.

The 2026 Hormuz Crisis Timeline

On 28 February 2026, the US and Israel launched what major international-law commentary described as an illegal attack on Iran. Reuters reported that the strikes killed Supreme Leader Ali Khamenei in the opening phase. Iran then retaliated with missiles, drones and restrictions on shipping through the Strait of Hormuz.

On 19 March, the US launched an aerial campaign to reopen the strait.

On 13 April, Washington imposed a naval blockade on Iranian ports.

A ceasefire now exists on paper. The strait is partly open. Ships are still delayed. Insurance is still expensive. Energy markets still carry a war premium.

That is not peace.

That is a pause with a price tag.

The Oil Price Picture

| Market point | Data |

|---|---|

| Normal Hormuz flow | ~20 mb/d |

| IEA 2026 supply decline | 3.9 mb/d |

| Brent high on 7 April | $138/bbl |

| Brent average in April | $117/bbl |

| EIA Brent estimate, May and June | ~$106/bbl |

| EIA Brent estimate, Q4 2026 | ~$89/bbl |

This table is the whole market problem.

The EIA’s baseline assumes traffic through Hormuz gradually resumes and shut in production comes back. That is why Brent falls toward $89 by Q4.

But if the recovery is slower, that forecast breaks.

The market is not only pricing oil.

It is pricing time.

Applying the 3D Framework

-

Direction: Oil remains supported. The IEA projects global oil supply to fall by 3.9 million barrels per day on average in 2026, even assuming Hormuz flows gradually resume. That is not a small fear premium. That is a physical supply problem.

-

Depth: Hormuz is the world’s most concentrated energy chokepoint. Saudi Arabia and the UAE have bypass pipelines, but they do not replace normal Hormuz flows. China, India, Japan and South Korea cannot reroute geography.

-

Downside: The real risk is duration. Not one dramatic spike. Not one headline. The danger is a slow grind where the strait remains unstable, LNG prices stay high, tanker routes stay distorted and energy inflation refuses to die.

Control Is the Prize

The US imports relatively little oil through Hormuz. That makes the situation clearer, not cleaner.

This is not mainly about American fuel.

Hormuz gives leverage over China, India, Japan, South Korea and Europe. It gives leverage over oil prices, LNG prices, shipping insurance, Asian manufacturing costs and global inflation.

That is why “access” is too soft a word.

The real fight is control.

Trump made that hard to hide when he said the US could open the Strait of Hormuz, take the oil and make a fortune.

That is not neutral language.

That is power language.

The US and Israel started the war. Iran then used the strait as leverage. Now households, workers and businesses around the world are paying the bill.

That is the honest chain.

The Law Is Not a Footnote

The 28 February US and Israeli strikes were not authorised by the UN Security Council.

They did not meet a convincing Article 51 self defence standard.

Major international law commentary described the strikes as manifestly illegal under Article 2(4) of the UN Charter.

That matters.

Not because international law stops powerful countries. It clearly does not.

It matters because the cost of breaking the law is now being exported into oil prices, LNG prices, supply chains and inflation.

The war was not free.

The bill arrived through energy markets.

Why Real People Pay

This is not only a trader’s problem.

A family in Europe pays more for heating.

A factory in India pays more for energy and feedstock.

A Japanese utility pays more for LNG.

A shipping company pays more for war risk insurance.

An airline either hedges perfectly or bleeds margin.

A small business gets told that transport costs have changed again.

The people who pay first are rarely the people who launch the missiles.

The Market Is Mispricing Time

The market wants a clean story.

Either the ceasefire holds and oil prices normalise.

Or the ceasefire breaks and Brent crude spikes.

That is too simple.

The more realistic outcome is slower and uglier.

Partial reopening. More inspections. More threats. More naval pressure. More insurance costs. More shipping delays. More diplomatic theatre.

Not full war.

Not full peace.

A slow grind.

That is the scenario markets often misprice because it is boring. It does not dominate television for one dramatic day. It just keeps raising costs.

Slow grind means Brent may stay higher for longer. It means LNG prices stay uncomfortable. It means tanker day rates remain elevated. It means central banks get another inflation problem just when they wanted to cut rates.

The mispricing is not only oil.

The mispricing is time.

Angles Worth Researching

Not recommendations. Research starting points.

Tanker stocks: Frontline, International Seaways, DHT and CMB.Tech are worth studying if disruption lasts longer than expected.

LNG stocks: Cheniere, Sempra and Woodside deserve attention if buyers pay more for supply outside the Gulf.

Defence stocks: Lockheed Martin, RTX and BAE Systems benefit from sustained military presence and munitions demand.

Brent options: Out of the money Brent calls for late 2026 can expire worthless. But they are worth understanding as insurance against a renewed oil price spike.

What to avoid: Airlines without strong fuel hedges, chemical producers dependent on Gulf feedstock, import heavy emerging markets and consumer businesses exposed to higher energy costs.

Takeaway

The Strait of Hormuz crisis is about power, law, geography and cost.

But responsibility is not equal.

The US and Israel launched an attack on Iran that major international-law commentary described as illegal. Iran then used the world’s most important energy chokepoint as leverage. The US now wants control over how the strait reopens. Europe wants energy security without paying the full political cost. Asian importers want flows restored before factories and consumers absorb more damage.

The cost is not shared equally.

The people who pay first are rarely the people who launch the missiles.

They are shipping crews, workers, commuters, airlines, factories, households and small businesses.

For investors, the clean question is this:

Is your portfolio built for a quick peace headline, or for a slow grind that keeps energy expensive for longer?

The market is leaning toward the first.

The evidence points toward the second.

The hunt is real. The strait is real. The mispricing is probably duration.

The takes on social media, mostly, are not.

Risk Notes

This post discusses an ongoing armed conflict. Facts on the ground change daily. Oil prices, ceasefire status, blockade status, shipping flows and legal interpretations may change after publication.

Nothing here is financial, investment, tax or legal advice. The specific tickers and instruments named are research starting points, not recommendations. Do your own due diligence and speak with a licensed advisor before committing capital.

Oil markets are unforgiving in geopolitical crises. Leverage, options and concentrated single name energy bets can produce large losses in either direction on one headline.

Be careful what you read. Be more careful what you believe. Be most careful what you trade on.

Found this useful?

Source note: IEA Oil Market Report May 2026, EIA Short Term Energy Outlook May 2026, Reuters, Chatham House, EJIL:Talk!, Dallas Fed, Al Jazeera, UNCTAD.

Disclosure: SCAD3D Insights holds no position in oil futures, tanker stocks, energy ETFs, LNG stocks or related instruments at the time of publication.

More Insights

Broadcom Drops 14%: Is the AI Market Rotation Real?

Broadcom dropped 14% on 4 June after beating earnings. Nvidia is up 19% YTD while AMD is up 143%. Is this the start of AI market rotation, or just a buy-the-dip moment?

- Broadcom

- AVGO

- AI Market Rotation

- AI Stocks

- Nvidia

- AMD

- AI Chip Selloff

- Priced for Perfection

- Sector Rotation

- Stock Market 2026

- AI Bubble

- IPO Supply

NVIDIA vs Dell: The AI Infrastructure Trade Explained

NVIDIA captures the highest-margin layer of the AI boom. Dell shows how much of that demand is becoming real servers, racks and data-center infrastructure.

- NVIDIA

- NVDA

- Dell

- DELL

- AI Infrastructure

- AI Servers

- Data Centers

- Semiconductors

- AI Chips

- AI Compute

Copper Market 2026: Supply Squeeze, EV Demand and How to Invest

Copper prices are rising because the world needs more electricity, EVs, grid upgrades and data centres, while supply remains tight. Here is the copper thesis in plain English.

- Copper

- Copper Price

- Copper Investing

- Copper ETF

- Copper Miners ETF

- CPER

- COPX

- Boliden

- Aurubis

- EV Demand

- Energy Transition

- China Copper Demand

- Copper Physical Premiums